Value For Our Country: Sustainable Economic Growth

Retail Banking

We Are There at Every Stage of Life

Ziraat Bank has adopted as a core approach providing solutions to financial needs encountered by individuals throughout their lives, from education to professional career and retirement, and has maintained its position aimed at supporting customers at every stage of their life.

The Bank supports its extensive nationwide physical presence with continuously developed digital infrastructure, offering a multi-channel service model for customer access. Products and services under the Retail Banking umbrella are accessible uninterruptedly through digital channels, enabling customers to carry out banking transactions independently of time and location.

Ziraat Bank, offering financial solutions for individual clients with an inclusive approach, significantly expanded its retail customer base throughout 2025. During the year, 2.7 million new retail customers were acquired, bringing the total number of retail customers to over 50 million, thereby maintaining its strong and leading position in the retail banking sector.*

Easy Access, Single Limit Solution

Launched last year to enable faster and more comprehensive responses to individual credit requests, the Easy Limit application consolidates the Overdraft Account (ODA), Credit Card, Consumer, and Auto Loan products under a single framework. The migration of the installation ODA product from branch channels to digital platforms, along with the introduction of the Digital Shopping Loan application, has expanded the range of individual credit products offered to customers through digital channels.

Maintaining its strong position in the housing finance sector, Ziraat Bank continued to support individual customers aiming to become homeowners in 2025, reinforcing its leading role in housing finance.

Digital Personal Loan Solutions and Customer Experience

Launched in 2024, digital personal loan solutions such as Easy Limit, ODA, and the Digital Shopping Loan continued to see increasing adoption by customers in 2025. By facilitating access to individual credit products through digital channels, these solutions have supported the shift of customer preferences toward digital platforms.

Integration of the credit application and disbursement processes has reduced screen transitions, shortened waiting times, and enhanced the overall customer experience. While consumer loan disbursements continued through digital channels, branch-based loan transactions also incorporated digital delivery of contract and document approvals, thereby reducing paper usage. These initiatives contributed both to operational efficiency and to improved customer satisfaction.

Management of the Personal Loan Portfolio and Current Trends

The personal loan portfolio is managed in line with the Bank’s sustainability vision, guided by principles of customer focus and efficient resource utilization. While the expansion of digital credit products has enhanced process efficiency, branch-based personal loan disbursements have also integrated customers into digital approval workflows.

As of 2025, the share of digital channels in individual credit demand has increased, with customers favoring faster, more transparent processes. In response, the Bank continues to manage its personal loan portfolio with a focus on digitalization and service quality.

Sustainability-Focused Personal Loan Products

Personal loan products supporting energy efficiency and environmental sustainability continued to occupy a significant place within the Bank’s retail banking activities in 2025. Through offerings such as the Energy Efficiency Management Loan, Individual Energy Efficiency Loan, Green Home Loan, Green Vehicle Loan, and TOGG-specific Vehicle Loan, the Bank has encouraged individual customers to invest in energy-saving solutions and low-carbon transportation alternatives.

Energy Efficiency Management Loan:

- This financing is provided to support investments aimed at improving the energy efficiency of buildings.

Individual Energy Efficiency Loan:

- It is extended to individual customers for the financing of their personal energy efficiency investments.

Green Housing Loan:

- In addition to the existing housing loan programs, the product is offered for high energy-efficiency residences to contribute to increasing the number of energy-efficient homes in Türkiye.

- In total, loans amounting to TL 79,391,864 were extended to 38 customers.

Green Vehicle Loan:

- This financing is provided for new vehicles based on the proforma/final invoice, and for used vehicles that are indicated as electric or hybrid on the vehicle registration certificate.

TOGG-specific Vehicle Loan:

- The program aims to support domestic production and promote low-carbon transportation.

- In total, loans amounting to TL 4.3 billion were extended to 5,721 customers.

Sustainability-oriented personal loan products are designed to help customers achieve both economic benefits and reduced environmental impact. While no new energy efficiency-focused personal loan products were introduced in 2025, demand for existing products continued, with a particularly notable increase in loans for electric vehicles. It is observed that sustainable finance instruments are becoming increasingly influential in individual customer preferences, and the Bank’s financing solutions aimed at reducing environmental impact have been well-received by retail customers.

Growth in Personal Loans

Ziraat Bank maintained its market share in personal loans in 2025, as it did in 2024, which constitute a significant portion of the Bank’s credit portfolio. In housing finance, the Bank disbursed TL 22.5 billion in 2024 and increased this to TL 59.3 billion in 2025. The Bank’s housing loan portfolio grew from TL 110 billion at the end of 2024 to TL 144 billion at the end of 2025, reflecting a 31% increase. In consumer loans, the Bank disbursed TL 89.7 billion in 2024, with an end-of-year total balance of TL 74.7 billion; in 2025, consumer loan disbursements reached TL 172.3 billion, with an end-of-year balance of TL 113 billion. For auto loans, the Bank disbursed TL 5 billion in 2024, achieving a total year-end balance of TL 8.3 billion; in 2025, with disbursements of TL 2.8 billion, the year-end balance reached TL 3.6 billion.

Financing of Locally Produced Vehicles

Individual auto loans aimed at supporting domestic production and promoting low-carbon transportation continued to be offered in 2025 within the framework of updated interest rates. Financing solutions specifically for domestically produced vehicles and TOGG aimed to facilitate customer access to these vehicles.

While contributed to the development of domestic industry, these loans also encouraged individual customers to opt for transportation alternatives with comparatively lower environmental impact. The Bank continues to maintain a sustainability- and domestic production-focused approach in its personal vehicle financing.

Increasing Product Ownership and Acquiring Active Customers

Within the scope of retail banking activities, efforts to increase product ownership among the existing customer base and to acquire customer segments that utilize Bank services at a limited level continued in 2025. Initiatives that encourage the use of various Bank products and services through the provision of credit products were implemented.

This approach, supported by interest rate improvements, aims to deepen customers’ engagement with the Bank’s products and increase active usage rates. Additionally, the integration of insurance products offered to individual customers into mobile and internet banking channels expanded the range of products and services available digitally, thereby simplifying customer access to the Bank’s offerings through a single platform.

Campaign Management and Effective Use of Digital Channels

In 2025, campaigns conducted within retail banking focused on encouraging customers to utilize credit products through digital channels. Campaigns structured via digital platforms have been observed to influence customer preferences toward these channels and contribute to increased digital banking usage.

The Bank aligns its campaign management with its digitalization strategy, aiming to enhance customer engagement and strengthen accessibility to retail banking services.

Total Payments of TL 24.2 Billion to 2.8 Million Pensioners5

5Customers choosing to recieve their retirement pensio from Ziraat Bank

Savings Incentive Products

The State-Supported Dowry Account and State-Supported Housing Account, developed in coordination with the Ministry of Family and Social Services and the Ministry of Treasury and Finance, continue to be offered to customers in line with Ziraat Bank’s objective of encouraging individual savings.

For these savings incentive products, applications for government contributions are submitted to the relevant Ministries for customers who make regular payments over a three-year period. Eligible customers receive the contribution amounts credited directly to their accounts. In the Foreign Exchange-Protected Deposit (KKM), designed to meet customer needs sensitive to foreign exchange fluctuations and to protect savings from currency volatility, the gradual reduction process continues.

The Advantage Term Deposit Account, launched in December 2024, allows customers to earn additional interest income based on their spending and payment transactions. Similar to the Uninterrupted Term Deposit Account, the Advantage Term Deposit Account enables withdrawals without waiting for the maturity date, without affecting the term of the account during transactions.

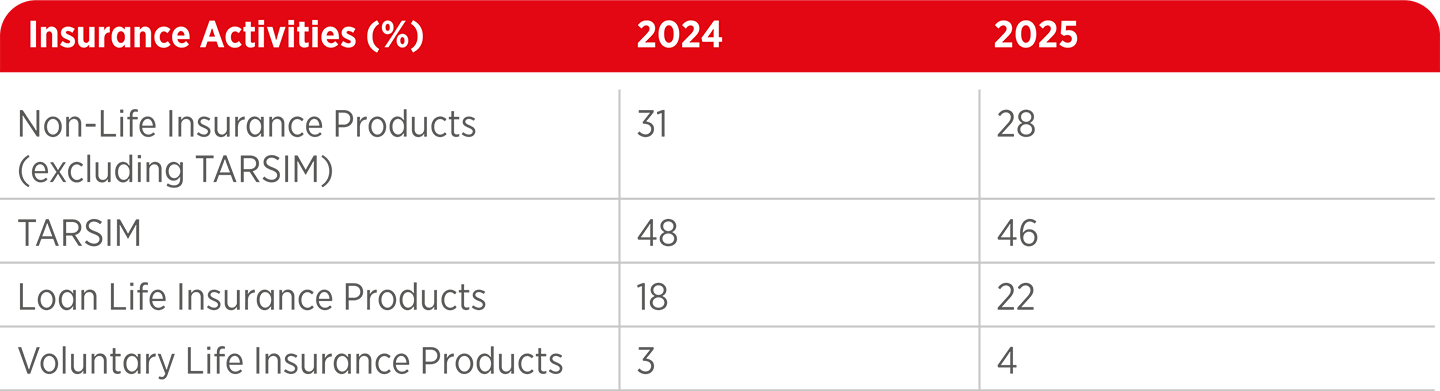

Insurance Activities

Ziraat Bank conducts its insurance brokerage activities in collaboration with Türkiye Sigorta A.Ş. and Türkiye Hayat ve Emeklilik A.Ş., while also expanding its operations through partnerships with Türkiye Katılım Sigorta A.Ş. and Türkiye Katılım Hayat A.Ş. This enables the Bank to operate as a comprehensive agency network covering both conventional and participation-based insurance through a total of four companies.

Through these partnerships, the Bank offers customers a broad portfolio that includes credit-linked life insurance, home insurance, Compulsory Earthquake Insurance (TCIP), motor vehicle insurance, traffic insurance, and TARSIM products, as well as optional life insurance, IPS, health insurance, personal accident coverage, engineering insurance, and other non-life insurance products.

In line with the objective of enhancing customer experience and accessibility, priority is given to offering insurance products via digital channels. By expanding product variety and simplifying processes, the Bank ensures fast and efficient service delivery.

The distribution of insurance activities reflects shifts in customer preferences within the portfolio. Non-life insurance products (excluding TARSIM) accounted for approximately 28% of the portfolio, while agricultural insurance maintained a strong position with a 46% share.

In contrast, the share of credit life insurance increased to 22%, indicating a heightened need for protection in credit processes. The share of voluntary life insurance reached 4%, demonstrating that individual customers are increasingly aware of the importance of long-term coverage.

Effective Cash Management Practices

Ziraat Bank provides customers with convenient, fast, and accessible payment options for invoices and other collections across hundreds of partner institutions. In addition to branch services, payments can be made via ATMs, Internet Banking, Mobile Banking, and Automatic Payment channels.

To support customers’ operational needs, the Bank continues to offer specialized payment solutions, magnetic check/bill processing, accounting integration, pooled accounts, and cash collection services.

The Easy Deposit service allows cash accumulated throughout the day in stores, branches, or dealerships to be deposited directly into the company’s main account via ATMs, quickly, securely, and free of charge, without the need for intermediaries, and continued to provide customers with privileged banking experience in 2025.

2026 and Beyond

Offering a comprehensive portfolio of products and services that address individual customers’ financial needs and expectations, Ziraat Bank aims to strengthen its customer-focused value proposition and establish sustainable, long-term relationships. Through its innovative product and service development approach, the Bank continues to operate with the goal of setting standards in retail banking, guiding the sector, and serving as a benchmark institution. For 2026, the Bank plans to:

- Expand the variety of individual credit products offered through digital channels and enhance service quality in these channels to guide customer preferences toward digital banking,

- Increase product ownership among existing individual customers to deepen engagement and implement initiatives to acquire customer segments that have not yet actively used Bank services,

- Enhance campaign activities to manage customer preferences more effectively and proactively,

- Continue offering vehicle loans for domestically produced vehicles at more favorable interest rates compared to other vehicle loans, in line with the Bank’s environmental and economic contributions,

- Sustain the offering of personal credit products that support energy efficiency.

The initiatives adopted in 2025 are intended to continue into 2026 and subsequent years.